Many people start budgeting with the idea that there must be a perfect formula. They search for a universal rule that tells them exactly how much to spend, save, and invest each month. While guidelines can be helpful, the truth is that the right budget is rarely a one size fits all solution. Every household has different priorities, obligations, and financial goals, which means the most effective budget is one that reflects those realities.

A good budget does not attempt to copy someone else’s financial structure. Instead, it works like a pesrsonal blueprint that adapts to your income, responsibilities, and lifestyle. When budgeting is approached this way, it becomes a flexible tool rather than a rigid system that feels difficult to maintain.

Many financial challenges also become easier to address once spending and obligations are clearly visible. For example, some households explore strategies like debt consolidation when they want to simplify multiple balances into one structured payment. When finances become easier to understand, it becomes much easier to design a budget that actually works.

The real purpose of a budget is not restriction. It is clarity.

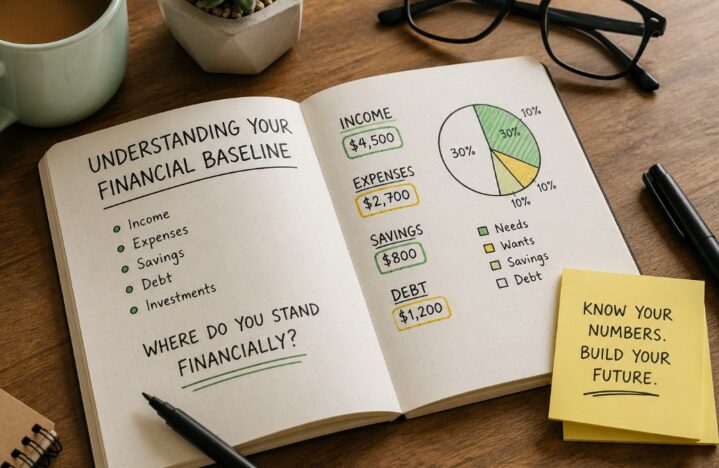

Start By Understanding Your Financial Baseline

Before building any type of budget, the most useful step is understanding your current financial situation. This means looking closely at your income, fixed expenses, and variable spending patterns. Without this baseline, it is difficult to create a plan that reflects reality.

A helpful way to begin is by identifying three main categories:

- Total monthly income after taxes

- Essential expenses such as housing, utilities, groceries, and transportation

- Discretionary spending such as dining out, entertainment, or shopping

When these numbers are clear, patterns begin to emerge. Many people are surprised to discover where their money is actually going each month. Small purchases that feel insignificant individually can add up quickly when repeated throughout the month.

Financial educators often emphasize the importance of understanding spending patterns before creating a budget. The Consumer Financial Protection Bureau provides tools that help individuals track income and expenses in order to build realistic financial plans.

Seeing your financial baseline clearly is the foundation of a budget that works long term.

Separate Needs From Wants Without Eliminating Enjoyment

One common budgeting mistake is trying to eliminate every non essential expense. While cutting spending can sometimes be necessary, an overly restrictive budget often fails because it removes too much flexibility from everyday life.

Instead, the goal is to distinguish between needs and wants while still allowing room for enjoyment.

Needs typically include expenses required for daily living and financial stability. These may include housing, utilities, food, transportation, insurance, and minimum debt payments. Wants, on the other hand, are expenses that enhance lifestyle but are not strictly necessary.

Examples of discretionary spending often include:

- Dining out or ordering takeout

- Subscription services

- Entertainment or travel

- Clothing beyond basic necessities

Recognizing these categories does not mean eliminating discretionary spending entirely. Instead, it allows you to choose how much of your income goes toward these experiences.

When budgeting reflects both responsibilities and enjoyment, it becomes much easier to follow consistently.

Align Your Budget With Your Personal Goals

A budget becomes much more meaningful when it reflects long term goals. Without goals, budgeting can feel like a series of restrictions rather than a path toward something valuable.

Personal goals vary widely depending on individual priorities. Some people focus on building an emergency fund, while others prioritize paying down debt, saving for a home, or preparing for retirement.

Common financial goals may include:

- Building three to six months of emergency savings

- Reducing outstanding debt balances

- Saving for education or major purchases

- Investing for long term financial growth

The Federal Reserve provides educational resources that explain how planning and saving contribute to financial stability over time. Their financial education materials can help individuals understand how budgeting supports broader financial goals. You can explore these resources at

When your budget clearly supports your goals, every financial decision begins to feel more purposeful.

Create A System That Is Simple To Maintain

One of the most important characteristics of a successful budget is simplicity. Complex financial systems may appear impressive, but they often become difficult to maintain during busy or stressful periods.

A simple budgeting system is easier to follow and easier to adjust when circumstances change.

Some people prefer using a basic spreadsheet, while others use budgeting apps that automatically track spending. Regardless of the method, the most important factor is consistency.

Simple budgeting systems often include a few key habits:

- Reviewing income and expenses at the beginning of each month

- Tracking major spending categories

- Setting aside money for savings and financial goals

- Adjusting spending as necessary throughout the month

These routines create awareness and allow you to respond to financial changes before they become larger problems.

Expect Your Budget To Evolve Over Time

Another important perspective is recognizing that a budget is not permanent. Life circumstances change, and financial plans must change along with them.

Income levels may shift due to career changes, new opportunities, or economic conditions. Expenses can also change as households grow, relocate, or take on new responsibilities.

Because of this, a budget should function as a living document rather than a fixed rulebook. Revisiting and adjusting your budget regularly helps ensure that it continues reflecting your current needs and goals.

Flexibility allows the budget to remain helpful rather than restrictive.

The Best Budget Is One You Will Actually Use

Ultimately, the right budget is not the one that looks perfect on paper. It is the one that fits your lifestyle and helps you make confident financial decisions.

A budget should provide guidance, not pressure. It should help you see where your money goes, support your financial priorities, and reduce the uncertainty that often surrounds personal finances.

When budgeting is approached as a tool for clarity and direction, it becomes much easier to maintain. Over time, the habits built through budgeting create a stronger financial foundation and a clearer path toward long term goals.

Defining the right budget is not about copying a formula. It is about creating a financial structure that works for your life.